Struggling with savings? This investment plan for NRI couples helps you build wealth, beat inflation, and retire stress-free.

Investment Plan for NRI Couples

If you’re a couple working abroad, earning well, saving decently… but still unsure whether you’re on track for retirement — you’re not alone.

Most people assume that earning in dinars automatically secures their future. But here’s the truth:

- High income doesn’t guarantee financial security.

- Without a proper investment plan for NRI couples, money slips away faster than expected.

And that’s where NRI retirement planning becomes crucial.

Think about it —

What happens when you return to India?

Will your savings be enough to sustain your lifestyle?

Let’s break it down step by step and build a powerful, practical, and realistic investment plan for NRI couples like you.

- Investment Plan for NRI Couples

- Why NRI Couples Need a Strategy

- India vs Gulf Lifestyle Comparison

- Retirement Corpus Calculation Formula

- Inflation Impact Explained

- Ideal Investment Plan for NRI Couples

- Best Mutual Fund Strategy for NRIs

- Step-by-Step Investment Plan for NRI

- Real-Life Case Study for Investment Plan for NRI

- Common Mistakes NRIs Make

- Best Strategy Summary

- FAQs

- Final Thoughts

- Disclaimer

Why NRI Couples Need a Strategy

Let’s be honest.

Life in Gulf is comfortable:

- Tax-free income

- High savings potential

- Stable job (mostly)

But…

👉 No pension

👉 No social security

👉 Limited long-term safety net

That’s why a structured investment plan for NRI couples is not optional — it’s essential.

And effective NRI retirement planning ensures:

- Financial independence

- Stress-free return to India

- Wealth creation beyond salary

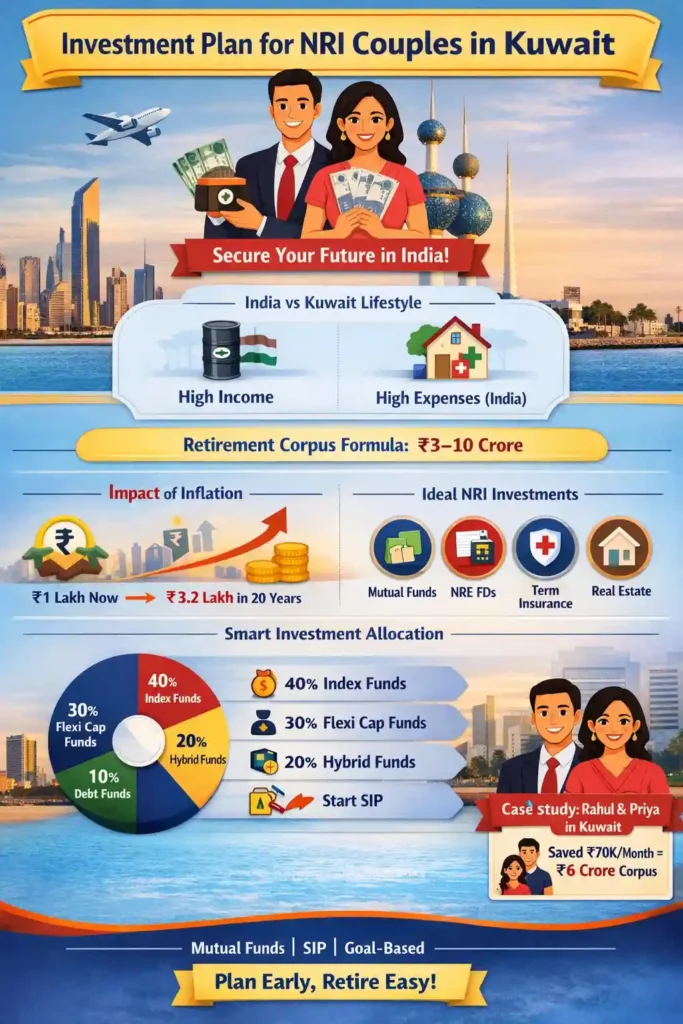

India vs Gulf Lifestyle Comparison

| Factor | GCC | India (Post Retirement) |

|---|---|---|

| Income | High | Zero / Limited |

| Expenses | Moderate | Increasing |

| Medical Cost | Employer covered | Self-funded |

| Lifestyle | Comfortable | Depends on savings |

👉 This is why NRI retirement planning must start early.

Retirement Corpus Calculation Formula

Here’s a simple way to estimate your retirement needs:

Formula:

Retirement Corpus = Annual Expenses × 25

Example:

- Monthly expense: ₹1,00,000

- Annual expense: ₹12,00,000

👉 Corpus required = ₹12,00,000 × 25 = ₹3 Crore

But wait…

This is where NRI retirement planning becomes more important.

Because…

👉 Inflation will increase this number significantly.

Inflation Impact Explained

Let’s assume inflation at 6%.

Example:

₹1 lakh today = ₹3.2 lakh in 20 years

So your ₹3 crore target becomes:

👉 ₹8–10 crore

This is why a strong investment plan for NRI couples is critical.

Ideal Investment Plan for NRI Couples

Now let’s get practical.

A solid investment plan for NRI couples should include:

1. Emergency Fund

- 6–12 months expenses

- Keep in NRE savings or liquid funds

2. Insurance

- Term insurance (India)

- Health insurance (India)

3. Mutual Funds (Core Strategy)

- Equity funds (long-term growth)

- Hybrid funds (balance)

4. Fixed Income

- NRE FD

- Debt funds

5. Goal-Based Investing

- Children education

- House

- Retirement

👉 This is the foundation of NRI retirement planning.

Best Mutual Fund Strategy for NRIs

Let’s simplify this.

Ideal Allocation:

| Category | Allocation |

|---|---|

| Index Funds | 40% |

| Flexi Cap Funds | 30% |

| Hybrid Funds | 20% |

| Debt Funds | 10% |

Why Mutual Funds?

- Rupee growth advantage

- Professional management

- Ideal for SIP

👉 A disciplined SIP is the backbone of any investment plan for NRI couples.

Step-by-Step Investment Plan for NRI

Let’s break this into action steps:

Step 1: Define Retirement Age

Example: 60 years

Step 2: Estimate Expenses

Factor inflation

Step 3: Calculate Corpus

Use formula

Step 4: Start SIP

Example:

- Monthly SIP: ₹50,000

- Expected return: 12%

- Time: 20 years

👉 Future Value ≈ ₹5 crore+

This is how NRI retirement planning works in reality.

Real-Life Case Study for Investment Plan for NRI

Meet Rahul & Priya 👇

- Age: 35

- Combined income: ₹3 lakh/month

- Savings: ₹1 lakh/month

They started:

- SIP: ₹70,000

- Duration: 20 years

Result:

👉 Corpus ≈ ₹6–7 crore

This is the power of a structured investment plan for NRI couples.

Common Mistakes NRIs Make

Let’s be real — most people fail because of these:

- Keeping money idle in savings

- Over-investing in real estate

- Ignoring inflationNo diversification

- No clear NRI retirement planning strategy

Avoid these, and you’re already ahead.

Best Strategy Summary

If you remember just one thing:

👉 Start early

👉 Invest consistently

👉 Focus on mutual funds

That’s the core of NRI retirement planning.

If you’re an NRI planning retirement and want a personalized investment plan for NRI couples, feel free to connect with me.

I can help you:

- Calculate your retirement corpus

- Build a mutual fund portfolio

- Optimize your NRI investments

FAQs

1. What is the best investment plan for NRI couples?

A mix of mutual funds, fixed income, and insurance is the best investment plan for NRI couples.

2. How much should NRI couples save for retirement?

Ideally, 20–30 times annual expenses should be saved under NRI retirement planning.

3. Can NRIs invest in mutual funds in India?

Yes, NRIs can invest through NRE/NRO accounts easily.

4. Is SIP good for NRI couples?

Yes, SIP is one of the best tools in any investment plan for NRI couples.

5. When should NRI retirement planning start?

As early as possible — ideally from your first job abroad.

Final Thoughts

Your Gulf income is powerful — but only if you use it wisely.

A proper investment plan for NRI couples can turn your earnings into long-term wealth.

And with the right NRI retirement planning, you won’t just retire…

👉 You’ll retire with confidence.

Disclaimer

Mutual Fund investments are subject to market risks. Please read all scheme-related documents carefully. Consult a financial advisor before investing.