NRI monthly income to parents made easy with SWP. Learn tax-efficient strategies, examples, and retirement planning tips for NRIs.

NRI Monthly Income to Parents: Tax-Free Strategy Explained

Introduction

If you’re an NRI, you’ve probably faced this situation…

Every month, you send money back home to support your parents. Sometimes ₹10,000, sometimes ₹25,000—depending on expenses. But have you ever thought:

- Is there a smarter way to create a fixed monthly income for parents?

- Can this be done in a tax-efficient way?

- What happens if one day you’re unable to send money?

This is where the concept of NRI monthly income to parents becomes important.

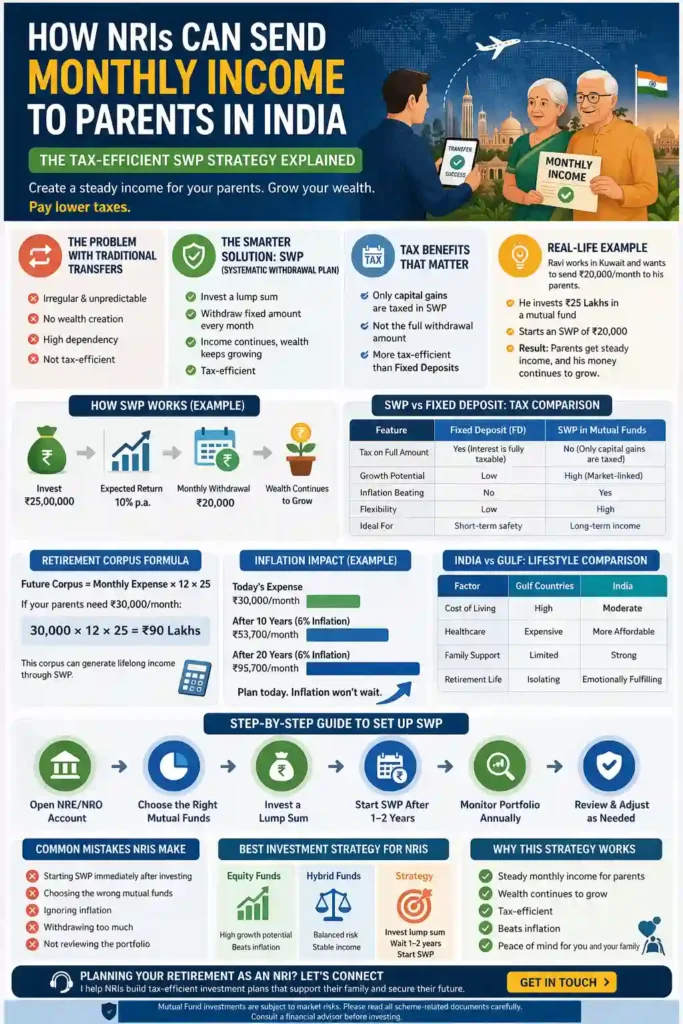

Instead of random transfers, you can create a structured, reliable, and tax-efficient income stream using a strategy called SWP (Systematic Withdrawal Plan).

In this guide, we’ll break down everything you need to know—from real-life examples to retirement planning strategies.

- NRI Monthly Income to Parents: Tax-Free Strategy Explained

- Introduction

- 1. What is NRI Monthly Income to Parents Strategy?

- 2. Problems with Traditional Money Transfers

- 3. What is SWP and How It Works

- 4. Tax Benefits Explained

- 5. Real-Life Example of NRI monthly income to parents

- 6. Retirement Planning for NRIs

- Retirement Corpus Formula

- 7. Inflation Impact

- 8. India vs Gulf Lifestyle Comparison

- 9. Best Investment Strategy

- 10. Step-by-Step Guide for NRI monthly income to parents

- 11. Common Mistakes NRIs Make

- 12. Advanced Strategy: Combine Goals

- FAQs

- Disclaimer

1. What is NRI Monthly Income to Parents Strategy?

The NRI monthly income to parents strategy is about creating a fixed, predictable income for your parents in India using investments instead of manual transfers.

Instead of sending money every month:

- You invest once (lump sum)

- Set up a withdrawal plan

- Parents receive a monthly income automatically

This ensures:

✔ Financial stability

✔ Independence for parents

✔ Peace of mind for you

2. Problems with Traditional Money Transfers

Let’s be honest…

Most NRIs:

- Send money randomly

- Depend on salary cycles

- Don’t plan long-term

Key Issues:

- No consistency

- No wealth creation

- High dependency

- No tax efficiency

Therefore, relying only on transfers isn’t sustainable.

3. What is SWP and How It Works

SWP (Systematic Withdrawal Plan) allows you to:

- Invest a lump sum in mutual funds

- Withdraw a fixed monthly amount

👉 Think of it like a salary for your parents

Example:

| Investment | Return | Monthly Withdrawal |

|---|---|---|

| ₹20 Lakhs | 10% | ₹15,000 |

Even after withdrawal, your investment continues to grow.

4. Tax Benefits Explained

This is where NRI monthly income to parents strategy becomes powerful.

👉 In SWP:

- Only capital gains are taxed

- Not the full withdrawal

Compared to FD:

| Investment | Tax Treatment |

|---|---|

| Fixed Deposit | Full interest taxable |

| SWP | Only gains taxed |

Therefore, SWP is more tax-efficient.

5. Real-Life Example of NRI monthly income to parents

Ravi, working in Kuwait, sends ₹20,000 monthly.

Instead, he:

- Invests ₹25 Lakhs

- Starts SWP of ₹20,000

Result:

✔ Parents get a steady income

✔ Investment grows

✔ Reduced tax

6. Retirement Planning for NRIs

Here’s where we introduce SEO keywords:

👉 NRI retirement planning India

Many NRIs ignore long-term planning.

But think:

“What happens after retirement?”

Retirement Corpus Formula

Future Corpus = Monthly Expense × 12 × 25

If parents need ₹30,000/month:

👉 30,000 × 12 × 25 = ₹90 Lakhs

7. Inflation Impact

Inflation silently destroys wealth.

If expenses today = ₹30,000

After 10 years = ₹50,000+

Therefore, your NRI monthly income to parents must grow.

8. India vs Gulf Lifestyle Comparison

| Factor | Gulf | India |

|---|---|---|

| Cost of Living | High | Moderate |

| Healthcare | Expensive | Lower |

| Family Support | Limited | Strong |

Hence, planning in India is more sustainable.

9. Best Investment Strategy

For NRI monthly income to parents, the best options:

✅ Equity Funds

- Long-term growth

- Beats inflation

✅ Hybrid Funds

- Balanced risk

- Stable income

Strategy:

- Invest a lump sum

- Wait 1–2 years

- Start SWP

10. Step-by-Step Guide for NRI monthly income to parents

- Open NRE/NRO account

- Choose a mutual fund

- Invest a lump sum

- Set SWP

- Monitor annually

11. Common Mistakes NRIs Make

❌ Starting SWP immediately

❌ Choosing the wrong funds

❌ Ignoring inflation

❌ Over-withdrawing

12. Advanced Strategy: Combine Goals

Use NRI retirement planning India + SWP:

- Build a retirement corpus

- Generate monthly income

- Protect family

If you’re an NRI planning retirement, feel free to connect with me. I can help you create a personalised investment plan based on your goals.

FAQs

1. What is the best way for NRIs to send money to their parents?

The best way is using SWP in mutual funds to create a fixed monthly income.

2. Is SWP tax-free in India?

Not fully tax-free, but only capital gains are taxed, making it tax-efficient.

3. Can NRIs invest in mutual funds in India?

Yes, NRIs can invest through NRE/NRO accounts.

4. How much should NRIs invest for monthly income?

It depends on expenses, but typically ₹20–30 lakhs can generate ₹15,000–₹20,000.

5. Is SWP better than fixed deposits?

Yes, SWP offers better returns and tax efficiency.

Disclaimer

Mutual Fund investments are subject to market risks. Please read all scheme-related documents carefully. Consult a financial advisor before investing.