NRI market crash mistakes can destroy retirement wealth. Learn retirement planning for NRIs and NRI retirement corpus planning strategies.

NRI Market Crash Mistakes: Why NRI Investors Panic More During Indian Market Crashes — Here’s the Data

Most investors think market crashes destroy wealth.

That’s not true.

The real wealth destroyer is often investor behavior.

And when it comes to NRI Market Crash Mistakes, the numbers tell an interesting story.

Many NRIs working in Kuwait, UAE, Saudi Arabia, Qatar, Oman, the UK, and the US earn excellent incomes. Yet surprisingly, many struggle to build the retirement wealth they expected.

Why?

Because during market crashes, they often react emotionally.

They stop SIPs.

They redeem investments.

They move to cash.

Then they miss the recovery.

If you’re serious about retirement planning for NRIs and effective NRI retirement corpus planning, understanding these behavioral mistakes could be worth crores over your lifetime.

- NRI Market Crash Mistakes: Why NRI Investors Panic More During Indian Market Crashes — Here's the Data

- Why NRIs Panic More During Market Crashes

- What the Data Reveals

- The Psychology Behind NRI Market Crash Mistakes

- Real-Life NRI Case Study

- Why Retirement Planning for NRIs Requires Emotional Discipline

- India vs Gulf Lifestyle Comparison

- Inflation: The Silent Wealth Killer

- Retirement Corpus Calculation Formula

- Common NRI Investing Mistakes

- Best Investment Strategy for NRIs

- Step-by-Step Retirement Planning Guide for NRIs

- Internal Linking Suggestions

- Key Takeaways

- Frequently Asked Questions

- Why do NRI investors panic during market crashes?

- What is the ideal retirement corpus for an NRI?

- Should NRIs stop SIPs during market crashes?

- Are mutual funds good for NRI retirement planning?

- How often should NRIs review their investments?

- What is the biggest retirement planning mistake NRIs make?

- Sources

Why NRIs Panic More During Market Crashes

Imagine this.

You are working in Kuwait.

Your family is in Kerala.

Oil prices are falling.

The rupee is moving.

The Indian market is down 20%.

Social media is filled with panic.

WhatsApp groups predict disaster.

What happens?

Fear takes over.

This is exactly where many NRI Market Crash Mistakes begin.

Unlike resident Indians, NRIs face multiple stress factors simultaneously:

- Currency fluctuations

- Job insecurity abroad

- Family responsibilities in India

- Geopolitical concerns

- Visa uncertainty

- Market volatility

As a result, market declines often feel much worse than they actually are.

What the Data Reveals

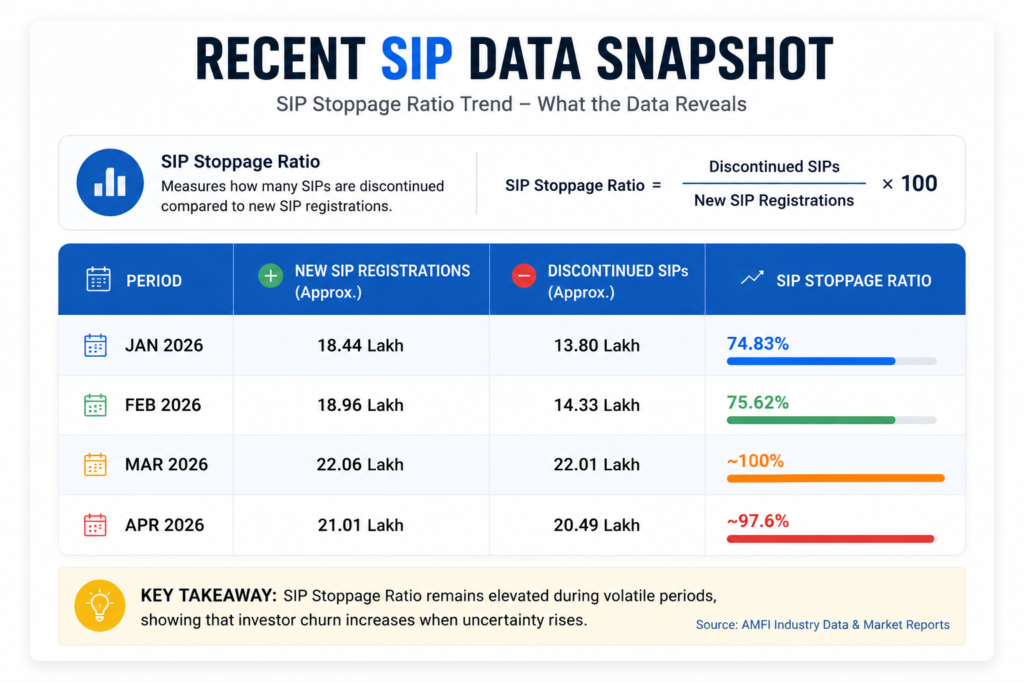

One interesting indicator is the SIP Stoppage Ratio.

The SIP Stoppage Ratio measures how many SIPs are discontinued compared to new SIP registrations.

Formula:

SIP Stoppage Ratio = (Discontinued SIPs ÷ New SIP Registrations) × 100

Recent AMFI-related data shows SIP stoppage ratios frequently remaining elevated, often above 70% and at times approaching or exceeding 100% during volatile periods. This indicates that investor churn rises significantly when uncertainty increases.

Recent SIP Data Snapshot

Source: AMFI industry data and market reports.

The message is simple.

Investors often become less disciplined when markets become volatile.

This directly impacts both retirement planning for NRIs and long-term NRI retirement corpus planning.

The Psychology Behind NRI Market Crash Mistakes

Most investors believe they’re rational.

Research suggests otherwise.

When markets fall:

- Fear increases

- News consumption increases

- Long-term thinking decreases

This creates a dangerous cycle.

Market falls → Fear rises → SIP stops → Recovery missed

The problem is not the crash.

The problem is the reaction.

This is one of the most common NRI Market Crash Mistakes.

Real-Life NRI Case Study

Let’s compare two investors.

Investor A: The Panic Investor

Age: 35

Location: Kuwait

Monthly SIP: ₹50,000

Behavior:

- Stops SIP during crashes

- Redeems investments

- Waits for recovery

Investor B: The Disciplined Investor

Age: 35

Location: Kuwait

Monthly SIP: ₹50,000

Behavior:

- Continues SIP

- Rebalances periodically

- Ignores short-term noise

Result After 20 Years

Assuming 12% annualized returns:

| Investor | Approx Wealth |

|---|---|

| Investor A | ₹4.9 Crore |

| Investor B | ₹7.2 Crore |

Difference:

₹2.3 Crore

That’s the hidden cost of NRI Market Crash Mistakes.

Why Retirement Planning for NRIs Requires Emotional Discipline

Most people think successful investing is about finding the best mutual fund.

Actually, successful retirement planning for NRIs is more about avoiding mistakes.

Consider this:

A market crash may last:

- 6 months

- 12 months

- 24 months

Retirement may last:

- 25 years

- 30 years

- 35 years

Which period matters more?

The answer is obvious.

Therefore, proper retirement planning for NRIs requires a long-term perspective.

India vs Gulf Lifestyle Comparison

Many Gulf NRIs underestimate retirement expenses.

Life in Gulf

- Company accommodation

- Tax-free income

- Transportation support

- Employer benefits

Retirement in India

- Medical expenses

- Domestic help

- Insurance costs

- Lifestyle inflation

- Family support obligations

Many people assume ₹50 lakh is enough.

Often it isn’t.

That’s why NRI retirement corpus planning becomes essential.

Inflation: The Silent Wealth Killer

Let’s examine a simple example.

Current monthly expense:

₹50,000

Assumed inflation:

6%

After 20 years:

Future Expense = Current Expense × (1 + Inflation)^Years

Future Expense = ₹50,000 × (1.06)^20

Future Expense ≈ ₹1,60,000 per month

That’s over 3 times higher.

This is why both retirement planning for NRIs and NRI retirement corpus planning must account for inflation.

Ignoring inflation is one of the biggest NRI Market Crash Mistakes.

Retirement Corpus Calculation Formula

A simple retirement calculation:

Annual Expense × 25

This follows the 4% withdrawal rule.

Example:

Required annual income:

₹24 lakh

Retirement Corpus:

₹24 lakh × 25

= ₹6 Crore

However, for conservative NRI retirement corpus planning, many advisors now recommend:

₹7–10 Crore

depending on lifestyle expectations.

Common NRI Investing Mistakes

Here are the biggest mistakes I repeatedly observe.

1. Stopping SIPs During Crashes

This is perhaps the costliest mistake.

2. Keeping Too Much Money in Savings Accounts

Inflation slowly destroys purchasing power.

3. Chasing Hot Stocks

Wealth is usually built through consistency.

4. No Retirement Goal

Without a target, investing becomes random.

5. Ignoring Asset Allocation

Many investors either take too much risk or too little.

6. Delaying Retirement Planning

The later you start, the harder retirement planning for NRIs becomes.

Best Investment Strategy for NRIs

For most investors, mutual funds remain one of the most efficient solutions.

Why?

Because mutual funds provide:

- Diversification

- Professional management

- SIP discipline

- Convenience

- Long-term wealth creation

A sample allocation:

| Asset Class | Allocation |

|---|---|

| Equity Mutual Funds | 60% |

| Hybrid Funds | 20% |

| Debt Funds | 10% |

| Emergency Fund | 10% |

The exact allocation depends on age, goals, and risk tolerance.

However, mutual funds play a central role in both retirement planning for NRIs and NRI retirement corpus planning.

Step-by-Step Retirement Planning Guide for NRIs

Step 1: Define Retirement Age

55?

60?

65?

Be specific.

Step 2: Estimate Future Expenses

Include:

- Housing

- Healthcare

- Travel

- Family support

Step 3: Calculate Retirement Corpus

Use inflation-adjusted projections.

Step 4: Build Emergency Fund

Maintain 6–12 months expenses.

Step 5: Start SIPs

Automate investing.

Step 6: Increase SIP Annually

Aim for:

10%–15% annual SIP increase.

Step 7: Review Portfolio Annually

Don’t review daily.

Review strategically.

Step 8: Stay Invested During Crashes

This single step can dramatically improve NRI retirement corpus planning outcomes.

Internal Linking Suggestions

To improve SEO and increase visitor engagement, create related articles:

- Best Mutual Funds for NRIs in 2026

- Retirement Planning for NRIs: Complete Guide

- NRE vs NRO Account Explained

- SIP vs Lump Sum for NRIs

- How Much Retirement Corpus Do NRIs Need?

- Inflation Planning for NRI Families

- Tax Planning for NRIs Investing in India

These supporting articles can strengthen your topical authority.

Key Takeaways

Why NRIs Panic More

- Multiple stress factors

- Distance from India

- Currency concerns

- Family expectations

What Data Shows

- SIP stoppage ratios rise during uncertainty

- Investor behavior matters more than market timing

- Long-term discipline wins

What Successful NRIs Do

- Continue SIPs

- Focus on goals

- Ignore market noise

- Follow structured retirement planning for NRIs

- Build systematic NRI retirement corpus planning

If you’re an NRI planning retirement and want clarity on your mutual fund strategy, retirement corpus requirements, or long-term wealth creation plan, feel free to connect with me.

Sometimes one conversation can help avoid years of costly investing mistakes.

Frequently Asked Questions

Why do NRI investors panic during market crashes?

NRIs often face additional pressures such as job uncertainty, currency fluctuations, family obligations, and geopolitical concerns. These factors can amplify fear during market declines.

What is the ideal retirement corpus for an NRI?

The answer depends on lifestyle and expenses. However, many NRIs may require ₹6–10 crore or more for a comfortable retirement in India.

Should NRIs stop SIPs during market crashes?

Generally, no. Continuing SIPs during market declines allows investors to purchase more units at lower prices and benefit from future recoveries.

Are mutual funds good for NRI retirement planning?

Yes. Mutual funds offer diversification, professional management, convenience, and long-term wealth creation potential, making them suitable for many NRI investors.

How often should NRIs review their investments?

An annual review is usually sufficient. Frequent monitoring often leads to emotional decisions.

What is the biggest retirement planning mistake NRIs make?

The biggest mistake is delaying retirement planning while assuming future income will solve everything. Early planning allows compounding to work effectively.

Sources

- AMFI Monthly Data

- AMFI and industry SIP reports on registration, discontinuation, and SIP inflows.

Disclaimer: Mutual Fund investments are subject to market risks. Please read all scheme-related documents carefully. Consult a financial advisor before investing.