If you’re an NRI reading this, chances are retirement planning has crossed your mind at least once — maybe during a quiet evening after work in the Gulf, or while strolling through Indian news from the US or Europe. You earn abroad, spend abroad, but deep down, many of us still imagine retirement in India.So this topic, NPS for NRIs explained, will give you an insight in your life aboard.

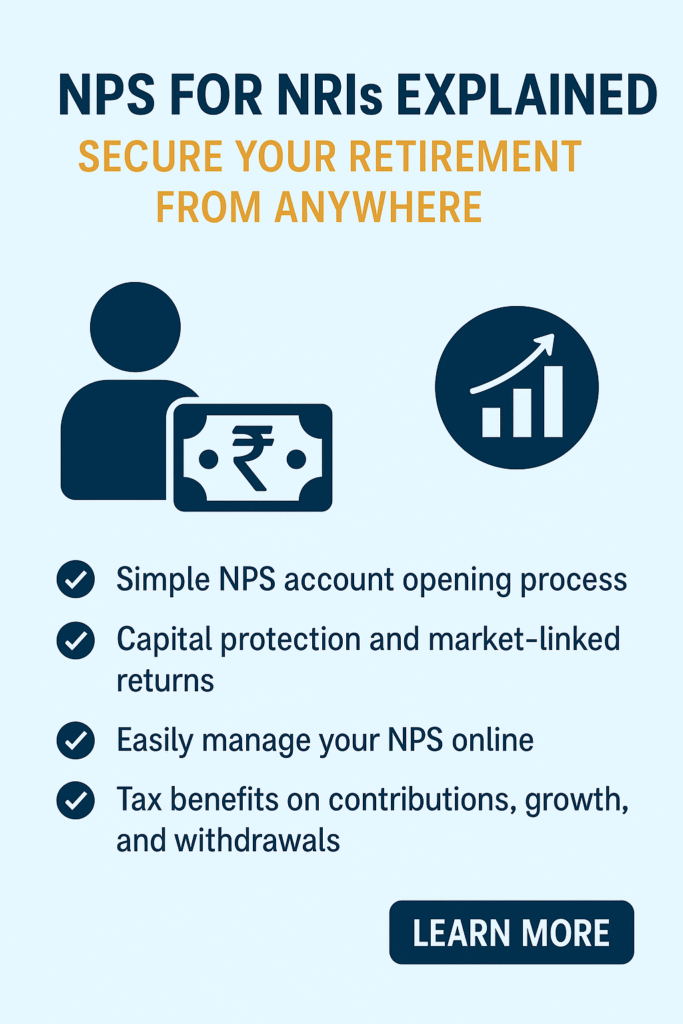

That’s exactly where NPS for NRIs explained becomes important. The National Pension System (NPS) is one of the most practical ways to secure your retirement from anywhere, even if you live thousands of kilometres away from India.

In this guide, I’ll break down NPS for NRIs explained in plain language — no textbook tone, no confusing jargon. Just honest, practical insights from one NRI to another. If your goal is to secure your retirement from anywhere, this article will give you clarity.

Table of Contents

- Why NRIs Should Think Seriously About Retirement in India

- What Is NPS? (Simple Explanation)

- NPS for NRIs Explained – The Big Picture

- Who Is Eligible for NPS as an NRI?

- Types of NPS Accounts for NRIs

- How NRIs Can Open an NPS Account from Abroad

- Contribution Rules NRIs Must Know

- Investment Options Inside NPS

- Auto Choice vs Active Choice for NRIs

- Returns: What Can NRIs Expect from NPS?

- Taxation of NPS for NRIs

- Withdrawal Rules at Retirement

- Annuity Options After Exit

- Repatriation Rules – Can NRIs Take Money Abroad?

- NPS vs Other Retirement Options for NRIs

- Real-Life NRI Example

- Common Mistakes NRIs Make with NPS

- FAQs – NPS for NRIs Explained

- Final Thoughts: Secure Your Retirement from Anywhere

1. Why NRIs Should Think Seriously About Retirement in India

Here’s a reality check.

Your job abroad won’t last forever. Residency rules change. Health priorities change. Parents age. Children settle. Suddenly, retirement feels closer than expected.

That’s why NPS for NRIs explained matters today, not at 55.

NPS allows NRIs to secure retirement from anywhere, build a rupee-based pension, and stay aligned with India’s growth story.

2. What Is NPS? (Simple Explanation)

NPS is a government-regulated retirement system managed by PFRDA. Think of it as a long-term pension account where you invest regularly and receive income after retirement.

When people ask about NPS for NRIs explained, this is the simplest way to put it:

You invest during your working years. NPS grows your money. At retirement, it pays you back as pension + lump sum.

That’s how you secure your retirement from anywhere.

3. NPS for NRIs Explained – The Big Picture

Let’s zoom out.

NPS for NRIs explained means:

- Long-term retirement planning in India

- Market-linked growth

- Low-cost structure

- Partial guaranteed income after retirement

For NRIs who want to secure retirement from anywhere, NPS acts as a stable backbone.

4. Who Is Eligible for NPS as an NRI?

NRIs can open NPS if:

- Age is between 18 and 70

- They comply with FEMA rules

- They have an NRE or NRO account

So yes, NPS for NRIs explained clearly — eligibility is broad and inclusive.

5. Types of NPS Accounts for NRIs

Tier I Account

- Mandatory retirement account

- Lock-in till 60

- Core of NPS for NRIs explained

Tier II Account

- Optional

- More flexible

- Not always available for NRIs

If your goal is to secure your retirement from anywhere, Tier I is non-negotiable.

6. How NRIs Can Open an NPS Account from Abroad

NRIs can open NPS:

- Online through eNPS

- Through authorised banks

Documents required:

- Passport

- PAN

- Overseas address proof

- NRE/NRO bank details

That’s the practical side of NPS for NRIs explained.

7. Contribution Rules NRIs Must Know

Minimum contribution:

- ₹500 per transaction

- ₹1,000 per year

There’s no upper limit — which makes it easier to secure retirement from anywhere, regardless of income level.

8. Investment Options Inside NPS

NPS invests in:

- Equity (E)

- Corporate Bonds (C)

- Government Securities (G)

This diversification is why NPS for NRIs explained is often recommended as a balanced retirement tool.

9. Auto Choice vs Active Choice for NRIs

Auto Choice

- Asset allocation changes with age

Active Choice

- You decide allocation

NRIs who want control prefer Active Choice. Both help you secure your retirement from anywhere.

10. Returns: What Can NRIs Expect from NPS?

Historically, NPS returns range between 9–12% annually.

Not guaranteed, but steady enough to make NPS for NRIs explained a serious long-term option.

11. Taxation of NPS for NRIs

Tax rules:

- Growth is tax-deferred

- Partial lump sum tax-free

- TDS applicable

Understanding tax is key to secure your retirement from anywhere.

12. Withdrawal Rules at Retirement

At age 60:

- Up to 60% lump sum

- Minimum 40% annuity

This structure is central to NPS for NRIs explained.

13. Annuity Options After Exit

Annuity provides:

- Monthly pension

- Lifetime income

This is where NPS truly helps secure retirement from anywhere.

14. Repatriation Rules – Can NRIs Take Money Abroad?

- NRE contributions: repatriable

- NRO contributions: subject to limits

Clear FEMA compliance keeps NPS for NRIs explained stress-free.

15. NPS vs Other Retirement Options for NRIs

Compared to FDs, mutual funds, or insurance:

- NPS is cheaper

- More structured

- Long-term focused

That’s why many experts say NPS for NRIs explained is essential reading.

16. Real-Life NRI Example

Ravi, an NRI in Dubai, started NPS at 38. Monthly contribution: ₹25,000. At 60, he expects a strong pension corpus — proof that you can secure your retirement from anywhere.

17. Common Mistakes NRIs Make with NPS

- Starting late

- Ignoring equity allocation

- Forgetting nomination

Avoid these to fully benefit from NPS for NRIs explained.

18. FAQs – NPS for NRIs Explained

Can NRIs invest in NPS?

Yes. NPS is open to eligible NRIs under FEMA.

Is NPS safe for NRIs?

Yes. It’s regulated and transparent.

Can NRIs secure retirement from anywhere using NPS?

Absolutely. That’s one of its biggest strengths.

19. Final Thoughts: Secure Your Retirement from Anywhere

Retirement isn’t about stopping work. It’s about freedom.

With NPS for NRIs explained clearly and implemented early, you can genuinely secure your retirement from anywhere — whether you’re in the Gulf today or back in India tomorrow.

Start early. Stay consistent. Let NPS quietly do its job.

Disclaimer: This content is for educational purposes only and does not constitute financial advice. Please consult a SEBI-registered advisor before investing.