Discover the best NRI Monthly Investment Plan and smart Investment Plan for NRI with ₹1 Lakh Salary to build wealth through SIPs, stocks, and retirement planning.

NRI Monthly Investment Plan for ₹1 Lakh Salary

If you are an NRI earning around ₹1 lakh every month, you are already in a strong financial position. However, income alone does not build wealth. A structured NRI Monthly Investment Plan does.

Many NRIs working in the Gulf or other countries earn well. Yet, surprisingly, they still struggle to create long-term wealth in India. Why does that happen?

Often, the reason is simple. There is no suitable investment plan for an NRI earning ₹1 Lakh. Money gets spent, transferred to family, or parked in savings accounts. As a result, the opportunity to grow wealth slowly disappears.

However, things change once you follow a disciplined NRI Monthly Investment Plan. With the right strategy, even a ₹1 lakh salary can create a multi-crore corpus over time.

So let’s explore how to design a powerful Investment Plan for NRI with ₹1 Lakh Salary step by step.

Table of Contents

- Why NRIs Need a Monthly Investment Plan

- How Much to Invest From ₹1 Lakh Salary

- Ideal Asset Allocation Strategy

- Best NRI Monthly Investment Plan Structure

- Mutual Funds Strategy for NRIs

- NPS for Retirement

- Stock Market Allocation

- Emergency Fund Planning

- Wealth Creation Example

- Common Mistakes NRIs Make

- Long Term Wealth Strategy

- FAQs

Why NRIs Need a Monthly Investment Plan

Most NRIs send money home regularly. Meanwhile, some invest in property. Others keep savings in bank deposits.

However, without a proper NRI Monthly Investment Plan, wealth building becomes slow and inconsistent.

A structured Investment Plan for NRI with ₹1 Lakh Salary helps in several ways.

First, it builds discipline. Every month, a portion of income gets invested automatically.

Second, it improves diversification. Instead of putting money into one asset, investments spread across different options.

Third, it reduces financial stress. Over time, a consistent NRI Monthly Investment Plan creates a solid financial cushion.

Therefore, planning is not optional. It is essential.

How Much Should NRIs Invest From ₹1 Lakh Salary

Now let’s address the most practical question.

How much should an NRI invest every month?

A simple rule works well for most people.

Invest at least 40% of income.

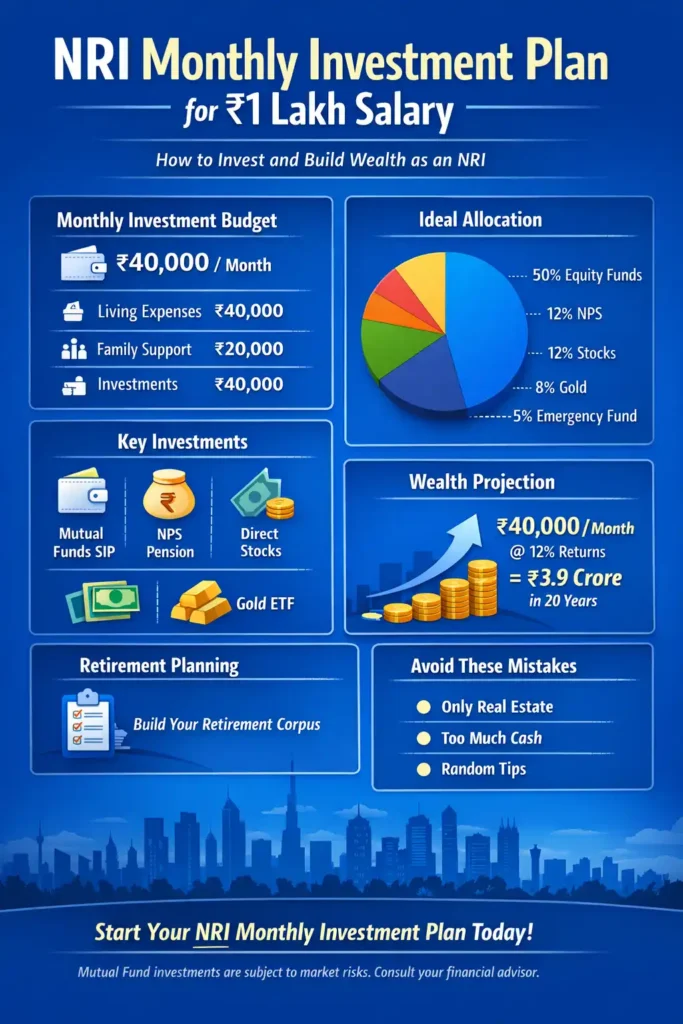

So if your income is ₹1,00,000, your Investment Plan for NRI with ₹1 Lakh Salary should invest about ₹40,000 per month.

Here is a simple example.

| Category | Monthly Amount |

|---|---|

| Living expenses | ₹40,000 |

| Family support | ₹20,000 |

| Investments | ₹40,000 |

This structure keeps finances balanced. At the same time, it allows your NRI Monthly Investment Plan to grow steadily.

Ideal Asset Allocation for NRIs

Diversification plays a major role in every successful Investment Plan for NRI with ₹1 Lakh Salary.

Markets move in cycles. Therefore, relying on a single investment type is risky.

Instead, a balanced NRI Monthly Investment Plan spreads money across several asset classes.

Example allocation:

| Investment Type | Monthly Investment |

|---|---|

| Equity Mutual Funds | ₹20,000 |

| Index Funds | ₹5,000 |

| NPS | ₹5,000 |

| Direct Stocks | ₹5,000 |

| Gold ETF | ₹3,000 |

| Emergency Fund | ₹2,000 |

This mix strengthens the overall Investment Plan for NRI with ₹1 Lakh Salary. It combines growth assets with stability.

Best NRI Monthly Investment Plan Structure

Now let’s turn theory into a practical NRI Monthly Investment Plan.

SIP in Mutual Funds – ₹20,000

Mutual funds form the backbone of most successful portfolios.

Therefore, they should dominate your Investment Plan for NRI with ₹1 Lakh Salary.

Advantages include:

• Professional management

• Diversification

• Long-term wealth creation

In addition, SIP investing removes emotional decisions. Markets may rise or fall. However, a disciplined NRI Monthly Investment Plan continues investing.

NPS Contribution – ₹5,000

Retirement planning often gets ignored. However, NRIs must think long term.

That is why adding NPS strengthens the Investment Plan for NRI with ₹1 Lakh Salary.

Key benefits include:

• Low cost structure

• Long-term retirement corpus

• Tax advantages

Over time, NPS becomes an important pillar of your NRI Monthly Investment Plan.

Direct Equity – ₹5,000

Direct stock investing can improve returns. However, discipline is important.

Instead of speculation, choose strong companies.

Examples include:

• Reliance Industries

• HDFC Bank

• TCS

When used wisely, equities enhance the Investment Plan for NRI with ₹1 Lakh Salary.

Gold Allocation – ₹3,000

Gold works as a financial safety net.

During market volatility, gold often performs well. Therefore, many investors include gold in their NRI Monthly Investment Plan.

Instead of jewellery, consider:

• Gold ETFs

• Sovereign Gold Bonds

Both options fit well within an Investment Plan for NRI with ₹1 Lakh Salary.

Emergency Fund – ₹2,000

Unexpected situations can occur. Job loss, medical emergencies, or travel needs may arise.

Therefore, every NRI Monthly Investment Plan should build an emergency fund.

Ideally, aim for six months of expenses.

This ensures your Investment Plan for NRI with ₹1 Lakh Salary remains stable even during difficult times.

Wealth Creation Example

Now let’s see the real power of compounding.

Suppose your NRI Monthly Investment Plan invests ₹40,000 every month.

Expected return: 12% annually

Investment period: 20 years

Future value:

| Monthly Investment | Total Wealth |

|---|---|

| ₹40,000 | ₹3.9 Crore |

That is the magic of a disciplined Investment Plan for NRI with ₹1 Lakh Salary.

Meanwhile, salary usually increases over time. As income grows, your NRI Monthly Investment Plan can invest even more.

Common Mistakes NRIs Should Avoid

Even a good Investment Plan for NRI with ₹1 Lakh Salary can fail if certain mistakes occur.

Here are common ones.

Investing Only in Real Estate

Many NRIs prefer property. However, property alone does not create diversification.

A proper NRI Monthly Investment Plan must include multiple asset classes.

Keeping Too Much Money in Savings Accounts

Savings accounts offer very low returns. Therefore, excess cash weakens your Investment Plan for NRI with ₹1 Lakh Salary.

Following Random Advice

Friends often recommend investments. However, their financial goals may be different.

Instead, follow a structured NRI Monthly Investment Plan aligned with your own goals.

Long-Term Strategy for NRIs

Consistency matters more than timing.

Markets will fluctuate. News will change. However, a disciplined NRI Monthly Investment Plan should continue without interruption.

Over time:

• Compounding accelerates

• Equity returns multiply

• Wealth grows steadily

Therefore, staying consistent with your Investment Plan for NRI with ₹1 Lakh Salary becomes the key to financial independence.

Final Thoughts

Earning ₹1 lakh every month is a strong starting point. However, real wealth appears only when income meets strategy.

A structured NRI Monthly Investment Plan transforms regular savings into long-term prosperity.

When you follow a disciplined Investment Plan for NRI with ₹1 Lakh Salary, you build:

• Financial independence

• Retirement security

• Wealth for future generations

Start early. Stay consistent. And let compounding work quietly in the background.

FAQs

Can NRIs invest in Indian mutual funds?

Yes. NRIs can invest in mutual funds using NRE or NRO accounts. Therefore, mutual funds often form the core of an NRI Monthly Investment Plan.

Is SIP good for NRIs?

Yes. SIPs provide disciplined investing. As a result, they are a key part of an Investment Plan for NRI with ₹1 Lakh Salary.

How much should NRIs invest monthly?

Most experts recommend investing 30–40% of income. This fits well into a strong NRI Monthly Investment Plan.

Can NRIs invest in Indian stocks?

Yes. NRIs can invest through NRE or NRO accounts using the PIS route. This helps diversify an Investment Plan for NRI with ₹1 Lakh Salary.

SEBI Disclaimer

Mutual Fund investments are subject to market risks. Please read all scheme related documents carefully before investing. The information provided in this article is for educational purposes only and should not be considered financial advice. Investors are advised to consult a qualified financial advisor before making investment decisions.