NRI retirement corpus in India explained. Learn how much retirement corpus NRIs need, how to calculate it, and the best investment strategy for retirement.

NRI Retirement Corpus in India: How Much Money Do NRIs Need to Retire Comfortably?

Every NRI dreams of one thing.

After years of working abroad, we want to return to India and live peacefully. Maybe in our hometown. Maybe close to family. Maybe near the beach or hills.

However, one big question always comes up.

What should be the NRI retirement corpus in India?

In other words, how much money do you actually need to retire comfortably in India?

Some people say ₹2 crore is enough.

Others say ₹5 crore.

Meanwhile, some financial planners recommend ₹10 crore.

So, which number is correct?

The truth is simple. There is no universal number. The required corpus in India depends on lifestyle, inflation, healthcare costs, and investment returns.

Therefore, this guide will help you understand:

- The ideal NRI retirement corpus in India

- How to calculate your retirement corpus

- Expenses NRIs face after retirement

- Inflation impact on retirement planning

- Smart investment strategies

Let’s break it down step by step.

- NRI Retirement Corpus in India: How Much Money Do NRIs Need to Retire Comfortably?

- Why Planning NRI Retirement Corpus in India Is Important

- NRI Retirement Corpus in India: How Much Do You Really Need?

- Factors That Decide Your NRI Retirement Corpus in India

- Example Calculation of Retirement Corpus in India

- Investment Strategies to Build NRI Retirement Corpus in India

- Common Mistakes in Planning NRI Retirement Corpus in India

- How Mutual Funds Help Build NRI Retirement Corpus in India

- FAQs on NRI Retirement Corpus in India

- Final Thoughts on NRI Retirement Corpus in India

Why Planning NRI Retirement Corpus in India Is Important

Most NRIs focus heavily on earning. However, many delay retirement planning.

At first, this may not look like a big problem. However, over time it becomes risky.

Here’s why planning your NRI retirement corpus in India early is extremely important.

Longer Life Expectancy

Today, many people live up to 85–90 years.

Therefore, retirement may last 25–30 years.

So your retirement corpus in India must support decades of expenses.

Rising Medical Expenses

Healthcare costs are rising quickly in India.

Moreover, medical inflation is often higher than normal inflation.

Therefore, the retirement corpus in India must include a buffer for medical emergencies.

Inflation Reduces Purchasing Power

Inflation quietly reduces the value of money.

For example, ₹1 lakh today may feel like ₹30,000 after 20 years.

Therefore, without planning, your retirement corpus in India may become insufficient.

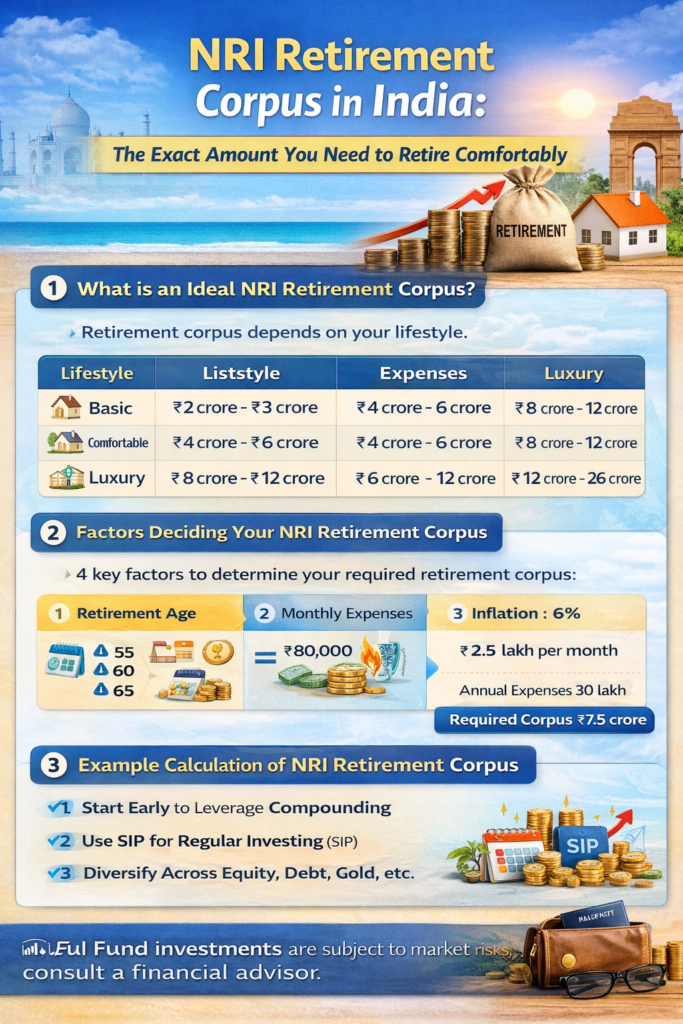

NRI Retirement Corpus in India: How Much Do You Really Need?

Let us address the most important question.

How large should the corpus in India be?

For most NRIs, retirement corpus depends mainly on lifestyle.

Here is a simple estimate.

| Lifestyle | Retirement Corpus |

|---|---|

| Basic | ₹2 crore – ₹3 crore |

| Comfortable | ₹4 crore – ₹6 crore |

| Luxury | ₹8 crore – ₹12 crore |

However, these numbers are only rough estimates.

Therefore, it is important to calculate your NRI retirement corpus in India using your own expenses.

Factors That Decide Your NRI Retirement Corpus in India

Several factors influence the required retirement corpus in India.

Let’s look at the most important ones.

Retirement Age and NRI Retirement Corpus

Retirement age directly affects the required corpus.

For example:

| Retirement Age | Retirement Years |

|---|---|

| 55 | 30 years |

| 60 | 25 years |

| 65 | 20 years |

Therefore, early retirement requires a larger NRI retirement corpus in India.

Monthly Expenses and Retirement Corpus in India

Your lifestyle determines expenses.

Typical retirement expenses include:

- Food and groceries

- Utilities

- Healthcare

- Travel

- Domestic help

- Insurance

For example:

| Expense Category | Monthly Cost |

|---|---|

| Living expenses | ₹40,000 |

| Healthcare | ₹15,000 |

| Lifestyle | ₹20,000 |

| Other expenses | ₹10,000 |

Total monthly expense = ₹85,000.

Therefore, annual expenses become about ₹10 lakh.

Consequently, this directly affects the required NRI retirement corpus.

Lifestyle Expenses and Retirement Corpus in India

Many NRIs underestimate retirement costs.

However, lifestyle plays a major role.

Typical monthly expenses may look like this.

| Lifestyle | Monthly Expense |

|---|---|

| Basic | ₹50,000 |

| Comfortable | ₹1 lakh |

| Premium | ₹2 lakh |

Therefore, a higher lifestyle requires a larger retirement corpus in India.

Inflation Impact on NRI Retirement Corpus in India

Inflation is the biggest challenge in retirement planning.

For example, assume inflation is 6% per year.

Then expenses double approximately every 12 years.

Let us see an example.

| Years | Monthly Expense |

|---|---|

| Today | ₹80,000 |

| 10 years | ₹1.4 lakh |

| 20 years | ₹2.5 lakh |

Therefore, inflation dramatically increases the required corpus in India.

This is why retirement planning must consider inflation carefully.

Example Calculation of Retirement Corpus in India

Let’s understand this with a simple example.

Assume the following:

Age: 40

Retirement age: 60

Current monthly expense: ₹80,000

Inflation: 6%

By retirement, expenses may increase to roughly:

₹2.5 lakh per month.

Annual expense becomes:

₹30 lakh.

Now we apply the 25X rule.

Required corpus:

₹30 lakh × 25 = ₹7.5 crore

Therefore, the required corpus in India in this example is around ₹7.5 crore.

Investment Strategies to Build NRI Retirement Corpus in India

Building a retirement corpus requires discipline.

However, the right investment strategy can make the process easier.

Start Early to Build a Retirement Corpus

Starting early helps enormously.

Because of compounding, small investments grow significantly over time.

For example:

Investing ₹30,000 per month for 25 years may grow to ₹5 crore or more.

Therefore, early investing helps build a strong NRI retirement corpus in India.

Use SIP to Build NRI Retirement Corpus in India

Systematic Investment Plans (SIP) are popular among NRIs.

SIP offers several advantages.

- Regular investing

- Compounding benefits

- Rupee cost averaging

Therefore, SIP is an effective way to grow your NRI retirement corpus in India.

Diversify Investments for Retirement Corpus in India

Diversification reduces risk.

A balanced portfolio may include:

- Equity mutual funds

- Index funds

- Debt funds

- Real estate

- Gold

Therefore, diversification protects the retirement corpus from market volatility.

Common Mistakes in Planning NRI Retirement Corpus in India

Many NRIs make avoidable mistakes.

Let’s look at the common ones.

Overdependence on Real Estate

Many NRIs invest heavily in property.

However, property does not always generate regular income.

Therefore, relying only on property can weaken the retirement corpus in India.

Ignoring Inflation

Inflation silently reduces purchasing power.

Therefore, ignoring inflation may lead to an inadequate retirement corpus in India.

Delaying Investments

Many people postpone retirement planning.

However, delaying investments increases the required savings dramatically.

Therefore, early planning is critical for building the NRI retirement corpus in India.

How Mutual Funds Help Build NRI Retirement Corpus in India

Mutual funds are powerful wealth-building tools.

They offer:

- Professional fund management

- Diversification

- Long-term growth

Moreover, equity mutual funds have historically delivered strong returns over long periods.

Therefore, they can play an important role in building the retirement corpus.

FAQs on NRI Retirement Corpus in India

What is the ideal NRI retirement corpus in India?

The ideal NRI retirement corpus is usually 25–30 times annual expenses.

Is ₹5 crore enough retirement corpus in India?

For many NRIs, ₹5 crore may be sufficient. However, lifestyle and inflation must be considered.

What investment is best for NRI retirement planning?

A diversified portfolio including equity mutual funds, debt funds, and fixed-income instruments works well.

Final Thoughts on NRI Retirement Corpus in India

Retirement planning is one of the most important financial decisions for NRIs.

However, many people delay this planning.

Instead, it is better to calculate your NRI retirement corpus early and start investing consistently.

When you plan well, retirement becomes peaceful.

You can return to India confidently. You can enjoy family, travel, and life without financial stress.

Therefore, start planning your retirement corpus in India today.

Your future self will thank you.

Disclaimer

Mutual Fund investments are subject to market risks. Please read all scheme-related documents carefully before investing. Investors should consult a financial advisor before making investment decisions.