Learn how Step-Up SIP NRI retirement strategy helps build a ₹5 crore corpus. Simple guide, examples, and planning tips for NRIs.

Step-Up SIP NRI Retirement: A Smart Strategy for Long-Term Wealth Creation

If you’re an NRI working in the Gulf, this is important.

👉 Are you increasing your investments every year?

Most NRIs don’t.

They start a SIP. Then they forget it.

However, income increases. Expenses increase. But investments stay the same.

That’s where Step-Up SIP NRI retirement strategy changes everything.

It helps you grow wealth faster. Moreover, it ensures your future in India is secure.

Let’s understand this in a simple way.

- Step-Up SIP NRI Retirement: A Smart Strategy for Long-Term Wealth Creation

- What is Step-Up SIP NRI Retirement Strategy?

- Why Step-Up SIP NRI Retirement Strategy is Powerful

- Step-Up SIP NRI Retirement vs Regular SIP

- Real-Life NRI Case Study

- NRI Retirement Corpus India Calculation

- Inflation and Step-Up SIP NRI Retirement

- India vs Gulf Lifestyle Comparison

- Best Strategy: Mutual Funds for Step-Up SIP NRI Retirement

- Step-by-Step Step-Up SIP NRI Retirement Plan

- Common Mistakes in Step-Up SIP NRI Retirement

- Step-Up SIP Impact Example

- FAQs

- Disclaimer

What is Step-Up SIP NRI Retirement Strategy?

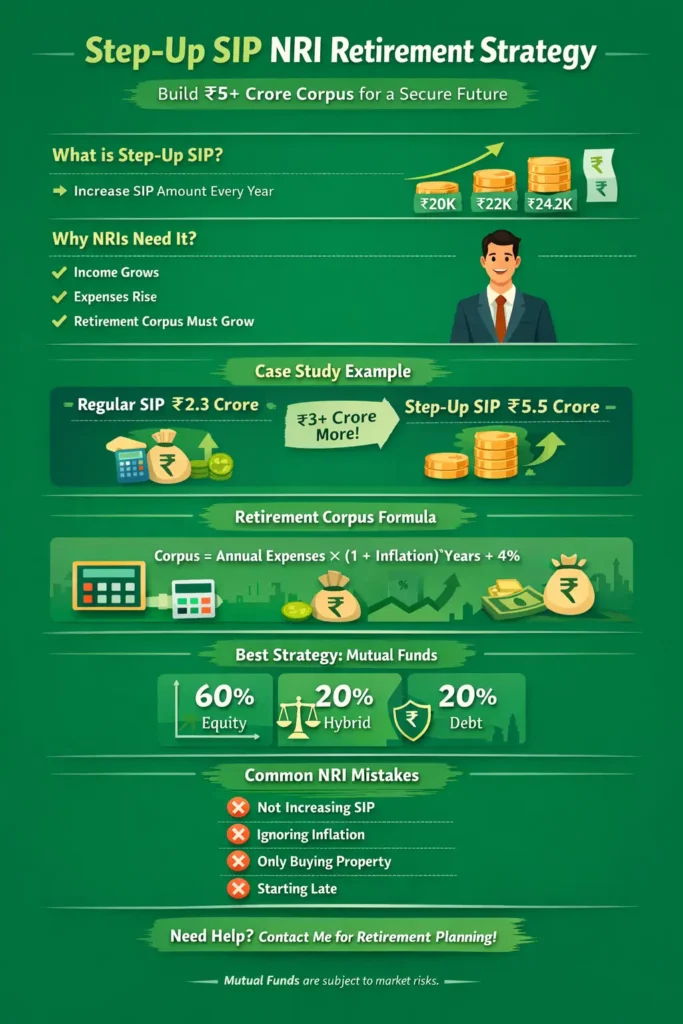

A Step-Up SIP NRI retirement strategy means increasing your SIP every year.

Instead of investing a fixed amount, you increase it gradually.

Example:

- Year 1: ₹20,000/month

- Year 2: ₹22,000/month

- Year 3: ₹24,200/month

So, your investment grows along with your salary.

Therefore, wealth creation becomes faster.

Why Step-Up SIP NRI Retirement Strategy is Powerful

NRIs usually earn more every year.

However, many fail to increase investments.

As a result, they miss huge wealth creation opportunities.

The Step-Up SIP NRI retirement method solves this problem.

Benefits:

- Matches salary growth

- Beats inflation

- Builds a large retirement corpus

- Ideal for long-term goals

Step-Up SIP NRI Retirement vs Regular SIP

| Feature | Regular SIP | Step-Up SIP NRI Retirement |

|---|---|---|

| Investment | Fixed | Increasing |

| Wealth | Limited | High |

| Inflation protection | Low | Strong |

Clearly, Step-Up SIP NRI retirement is better.

Real-Life NRI Case Study

Let’s take an example.

An NRI in Kuwait:

- Age: 30

- SIP: ₹20,000

- Step-Up: 10%

- Duration: 25 years

Without Step-Up SIP:

- Investment: ₹60 lakh

- Corpus: ₹2.3 crore

With Step-Up SIP NRI retirement:

- Investment: ₹1.8 crore

- Corpus: ₹5.5 crore

👉 Difference: ₹3 crore+

That’s the power of this strategy.

NRI Retirement Corpus India Calculation

This is very important.

Formula:

Retirement Corpus = Annual Expense × (1 + Inflation)^Years ÷ 4%

Example:

- Current expense: ₹6 lakh

- Inflation: 6%

- Years: 25

Future expense = ₹25 lakh

Corpus required = ₹6.25 crore

This is called NRI retirement corpus India calculation.

Inflation and Step-Up SIP NRI Retirement

Inflation reduces your money’s value.

For example:

- ₹50 today → ₹200 in future

- ₹25,000 rent → ₹1 lakh

Therefore, Step-Up SIP NRI retirement helps you stay ahead.

India vs Gulf Lifestyle Comparison

Life in the Gulf is different.

However, retirement happens in India.

Gulf:

- High income

- Low tax

India:

- Rising expenses

- Medical costs

Therefore, your Step-Up SIP NRI retirement plan must consider Indian expenses.

Best Strategy: Mutual Funds for Step-Up SIP NRI Retirement

Mutual funds are ideal.

Suggested Allocation:

- 60% Equity funds

- 20% Hybrid

- 20% Debt

Moreover, SIP + Step-Up works best in mutual funds.

Step-by-Step Step-Up SIP NRI Retirement Plan

Step 1: Fix retirement age

Step 2: Estimate expenses

Step 3: Do NRI retirement corpus India calculation

Step 4: Start SIP

Step 5: Activate Step-Up SIP

Step 6: Review yearly

Simple and effective.

Common Mistakes in Step-Up SIP NRI Retirement

Many NRIs make these mistakes:

- Not increasing SIP

- Investing only in real estate

- Ignoring inflation

- Starting late

Avoid these to succeed.

Step-Up SIP Impact Example

- SIP: ₹20,000

- Step-Up: 10%

- Duration: 20 years

| Type | Corpus |

|---|---|

| Regular | ₹2 crore |

| Step-Up SIP NRI retirement | ₹3.8 crore |

Huge difference.

FAQs

What is Step-Up SIP NRI retirement?

It is a SIP where you increase investment yearly to build wealth faster.

Is Step-Up SIP better than SIP?

Yes, because it grows with income.

How much should NRIs invest?

At least 20–30% of income.

How to calculate corpus?

Use NRI retirement corpus India calculation formula.

Is mutual fund good for NRIs?

Yes, it is one of the best options.

Disclaimer

Mutual Fund investments are subject to market risks. Please read all scheme-related documents carefully. Consult a financial advisor before investing.